The Complete Guide to Car Finance in South Africa

Everything You Need to Know Before You Sign on the Dotted Line

Buying a car is one of the biggest financial decisions most South Africans will ever make. And unless you have R300,000 sitting in a savings account, you're going to need car finance.

But here's the thing: car finance in South Africa isn't just about finding a bank that says "yes." It's about understanding how interest rates work, what the law allows (and doesn't allow), and how to protect yourself from predatory lenders.

I've put together this guide to walk you through everything—from how finance works to your legal rights as a consumer. No jargon, no fluff. Just practical information backed by actual court cases and the law.

Let's get started.

Part 1: How Car Finance Actually Works

The Basic Idea

Car finance is a loan that helps you buy a vehicle without paying the full price upfront . A bank or finance company pays the dealership on your behalf, and you repay that amount in monthly instalments—typically over 12 to 96 months.

Your monthly payment covers four things:

-

The capital (the actual cost of the car)

-

Interest (the bank's fee for lending you money)

-

Initiation fee (a once-off fee set by the National Credit Act)

-

Monthly service fee (charged for as long as the account is active)

Once you've made every payment, the car is yours. Simple enough, right? Well, not quite. The details matter.

The Main Types of Car Finance

1. Instalment Sale (Most Common)

This is the straightforward option. You pay off the car over an agreed period, and after the final payment, you own the vehicle.

Real example: Lerato finances a new Haval Jolion for R426,000 over 60 months at a fixed interest rate of 12%. She pays about R9,400 per month, and after 5 years, the car is hers .

Pros: You end up owning the vehicle

Cons: Monthly payments are higher without a balloon payment

2. Balloon Payment (Residual)

This is where things get interesting—and risky. A portion of the vehicle's price (usually 20-40%) is deferred to the end of the contract, which lowers your monthly payments.

Real example: Themba buys a GWM P300 for R600,000 with a 30% balloon (R180,000). His monthly payments drop to around R10,600—but he still owes R180,000 at the end of 5 years .

Pros: Lower monthly instalments

Cons: You face a massive lump sum payment at the end. If you can't pay it, you'll need to refinance (often at higher rates) or lose the car.

Important note: Balloon payments are only allowed on finance terms up to 84 months .

3. Guaranteed Future Value (GFV)

This is becoming more popular. The lender guarantees what your car will be worth at the end of the term. You then have three choices:

-

Trade it in for a new model

-

Pay the guaranteed amount to keep it

-

Return the car (subject to mileage and condition conditions)

Pros: You know exactly what you're dealing with

Cons: You must stick to mileage limits and service schedules

What You'll Need to Apply

Before you even walk into a dealership, get these documents ready. Banks won't consider you without them:

-

Valid SA ID and driver's licence

-

Latest 3 months' payslips

-

Latest 3 months' bank statements

-

Proof of address (not older than 3 months)

-

A decent credit record (generally starting from 670 on most scoring systems)

If you're self-employed and applying in your company's name, you'll also need business bank statements, audited financial statements, and company registration documents .

Part 2: How Banks Decide Your Interest Rate

Here's where most people get confused—and where a bad credit score can cost you tens of thousands of rands.

Your interest rate determines how much you'll actually pay for your car over time. And banks look at several factors to set that rate .

The Credit Score Factor

A higher credit score means lower perceived risk, which means a better interest rate. Simple.

If you've paid your accounts and loans on time, you'll likely qualify for a lower rate. If you've missed payments or defaulted, expect to pay more.

The Debt-to-Income Ratio

Banks calculate how much of your income is already committed to debt. If your monthly debt (including the new car payment) exceeds about 30-40% of your income, they may decline your application or adjust the rate higher .

The Deposit

Putting down a deposit shows commitment and reduces the bank's risk. It can improve your approval odds. However, here's a counter-intuitive fact: a large deposit can sometimes attract a higher interest rate because the principal debt is lower, so the bank earns less interest overall .

The Loan Term

Shorter terms (48 months vs. 72 months) can attract higher interest rates since the bank earns interest over a shorter timeframe. However, shorter periods result in lower overall interest charges—even if the rate is slightly higher .

The Car Itself

Banks prefer newer vehicles because they retain value better. Financing a brand-new car often comes with more competitive rates than older used cars. Special offers are typically only available on new vehicles .

Real Numbers: How Interest Rates Impact Your Wallet

Let's look at a concrete example. Sipho buys a new GWM Tank 300 for R800,000 over 60 months with no deposit .

Credit Profile Interest Rate Monthly Payment Total Paid Over 5 Years Excellent (Prime rate) 10.25% ±R17,200 R1,032,000 Average (Prime + 2%) 12.25% ±R17,900 R1,073,000 Poor (Prime + 6%) 16.25% ±R19,500 R1,168,000

The difference between excellent and poor credit? Over R136,000. That's not a small amount. That's a year's worth of groceries for a family.

This is why maintaining a good credit record is so important. A few missed payments years ago can cost you a fortune today.

Part 3: Current Interest Rates (2026)

As of March 2026, the South African Reserve Bank (SARB) has kept the repo rate at 6.75%, with the prime lending rate at 10.25% .

To give you context, here's how we got here:

Date Action Repo Rate Prime Rate March 2024 Held 8.25% 11.75% September 2024 Cut 25bp 8.00% 11.50% November 2024 Cut 25bp 7.75% 11.25% January 2025 Cut 25bp 7.50% 11.00% May 2025 Cut 25bp 7.25% 10.75% July 2025 Cut 25bp 7.00% 10.50% November 2025 Cut 25bp 6.75% 10.25% January 2026 Held 6.75% 10.25% March 2026 Expected to hold 6.75% 10.25%

The SARB has cut rates by 150 basis points from the 2024 peak . Inflation has fallen to 3.0% as of February 2026—hitting the new target midpoint for the first time .

What this means for you: If you have a linked interest rate (where your rate moves with the prime rate), your monthly payments have likely decreased over the past 18 months. If you have a fixed rate, your payments stay the same regardless of what the SARB does.

Part 4: Your Legal Rights Under the National Credit Act

This is the most important section of this guide. The National Credit Act (NCA) is your shield against unscrupulous lenders. And recent court cases have strengthened consumer protections significantly.

What the NCA Says About Fees

The NCA sets strict limits on what lenders can charge you. Section 101 lists the only costs a credit provider can require you to pay :

-

The principal debt (the amount you borrowed)

-

An initiation fee (capped by law)

-

A service fee (monthly or annually)

-

Interest (at a maximum prescribed rate)

-

Credit insurance costs

-

Default administration charges (only if you default)

-

Collection costs (capped by law)

Section 102 specifies what can be included in the principal debt for instalment agreements :

-

Initiation fee (if you choose to finance it)

-

Extended warranty costs

-

Delivery, installation, and initial fuelling charges

-

Taxes, licence, or registration fees

-

Credit insurance premiums

Important: This is a "closed list." Lenders cannot invent new fees or charges beyond what the NCA explicitly allows .

The Landmark "On the Road Fees" Case

In September 2025, the Supreme Court of Appeal (SCA) issued a major ruling about "On the Road" (OTR) fees—those extra costs like registration, licence plates, and pre-delivery inspections .

For years, there was confusion about whether lenders could finance these fees. The National Credit Regulator (NCR) argued they were "prohibited charges." Lenders argued they were just financing a deal already struck between you and the dealer.

The SCA's ruling: Yes, lenders can finance OTR fees—but only with full transparency .

The Court established three rules for all future deals :

-

Itemise everything: Each OTR component must be listed separately with its individual cost. No lumping into a vague "OTR total."

-

Choice is yours: The dealer must ask if you want to pay cash for these extras or finance them.

-

Show the maths: The dealer must reveal both the cash price and the financed total (including interest), so you can make an informed decision.

This is a huge win for consumers. No more hidden fees buried in the fine print.

The "In Duplum" Rule: Your Protection Against Unlimited Interest

Here's a rule every borrower should know: in duplum (Latin for "double").

This common-law principle states that interest on a loan stops running when the unpaid interest equals the amount of the outstanding capital . In simple terms: you'll never pay more than double what you originally borrowed.

The NCA later wrote this rule into law to prevent lenders from accumulating interest and fees beyond double the amount that was outstanding when you first defaulted .

Real example from an NFOSA case: A complainant borrowed R41,000 against a life insurance policy. The insurer had failed to apply the in duplum rule, allowing interest to accumulate beyond the legal limit. Once the rule was applied, the total debt was reduced from over R93,000 to R82,136—saving the borrower over R13,000 .

The Debt Review Victory (2025)

In a major 2025 High Court case (Chantelle Scott v National Credit Regulator and Others), the court ruled that banks cannot cancel a loan agreement once a consumer enters debt review .

The Banking Association of South Africa (Basa) had argued that entering debt review effectively cancels the original loan agreement—which would allow banks to charge higher interest and additional fees.

The court disagreed. The full bench of the Pretoria High Court ruled that applying for debt review does not cancel the original credit agreement. The in duplum rule continues to apply while consumers are under debt review .

The banks have appealed, but as of now, this is a significant protection for consumers struggling with debt.

What the Case Revealed About Bank Practices

The court case exposed some troubling practices by banks. Legal consultant Leonard Benjamin noted that banks have been "selling the homes of people when they are not, in fact, in default" .

One practice highlighted was "double-dipping" —where banks restructure arrears by spreading them over the remaining loan term (which should clear the default) but then continue to pursue legal action for the now non-existent arrears .

If you're under debt review, you should be aware of this. Your arrears may have been "purged" through recapitalisation, even if the bank is still chasing you for them.

The Loan Shark Case (2025)

The Supreme Court of Appeal also dealt a blow to predatory lenders in 2025. In National Credit Regulator v The Loan Company, the SCA upheld a R250,000 fine against a company operating as a "pawn broking" business .

The company had advanced R35,000 to a customer who put up his 2002 BMW (valued at R100,000) as security. When the customer defaulted on a R42,000 repayment, the company sold his car for R65,000 and kept the entire amount—not just the outstanding debt .

The court ruled this was unlawful. As Judge Phillip Coppin stated: "Commissary agreements were prohibited in Roman times because they were harsh, unjust and unfair. That prohibition has endured for centuries and still applies in SA law" .

What this means for you: Even if you default, a lender cannot simply take your asset and keep everything. They are only entitled to recover the actual amount owed—plus lawful charges.

Part 5: Protections for Lenders (Yes, They Have Rights Too)

The NCA isn't one-sided. While it strongly protects consumers, it also gives lenders legal recourse when borrowers don't meet their obligations.

Default and Repossession

If you miss payments, the lender can:

-

Charge default administration fees (capped by law)

-

Demand immediate repayment of the full outstanding balance

-

Repossess the vehicle (after following proper legal procedures)

However, the in duplum rule limits how much interest and fees can accumulate during default . Lenders cannot simply let interest run indefinitely.

The "On the Road Fees" Ruling Also Protected Lenders

While the SCA imposed transparency requirements, it also confirmed that lenders can legitimately finance OTR fees that are genuine costs of getting the car from the lot to your driveway . This ended years of legal uncertainty for the industry.

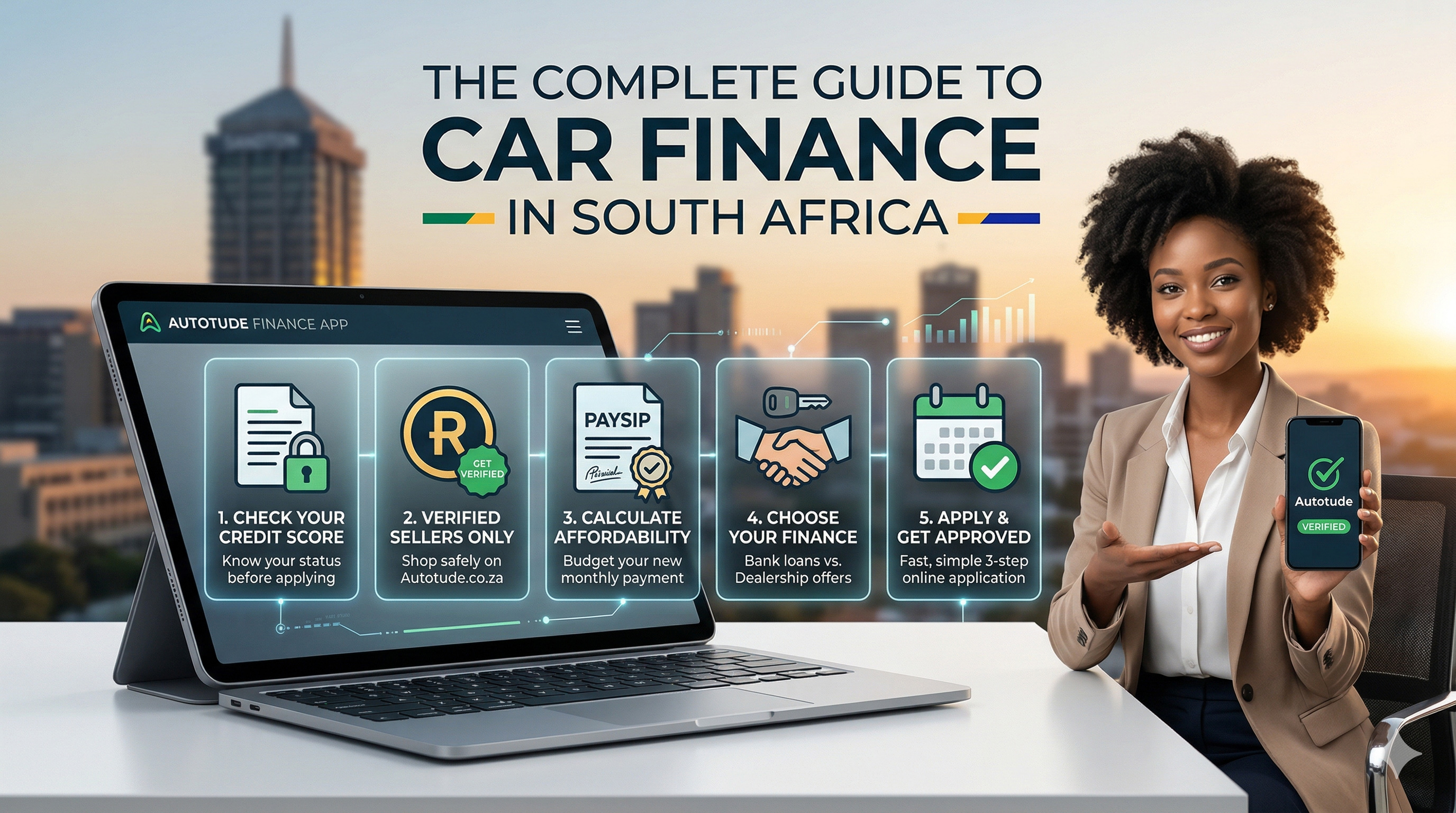

Part 6: Your Pre-Approval Checklist

Before you step into a dealership, do these five things:

1. Check Your Credit Score

Get a free credit report from TransUnion, Experian, or Compuscan. Know where you stand before a bank tells you. A score above 670 generally puts you in a good position .

2. Calculate Your Real Affordability

Don't just look at the monthly instalment. Consider:

-

Insurance (required for financed vehicles)

-

Fuel (based on your actual driving distance)

-

Maintenance (tyres, services, repairs)

-

Toll fees and parking

A good rule of thumb: if you can't comfortably afford double the instalment each month, you can't afford the car.

3. Save a Deposit

Even R10,000–R20,000 reduces your monthly payment and total interest significantly. It also shows the bank you're serious.

4. Get Pre-Approved

Walk into a dealership with pre-approval from your bank. This puts you in a stronger negotiating position and stops you from falling for "we can get anyone approved" dealership tricks.

5. Read Everything Before Signing

The NCA requires transparency, but you still need to read the fine print. Check for:

-

The interest rate (fixed or linked?)

-

The full term length

-

Any balloon payment amount

-

Early settlement penalties

-

Insurance requirements

Part 7: Red Flags to Watch Out For

"Guaranteed Approval" from a Dealership

No legitimate lender guarantees approval without checking your credit. If a dealership promises to get you financed regardless of your credit history, be very careful. They may be offering a loan at exorbitant rates or through an unregistered credit provider.

Pressure to Sign Quickly

Legitimate lenders want you to understand what you're signing. If someone is rushing you, walk away.

Fees That Aren't Listed

The NCA requires full disclosure of all fees. If a dealer adds "admin fees" or "processing fees" that aren't in the NCA's allowed list, that's a violation.

No Written Agreement

Verbal promises mean nothing. Get everything in writing before you pay a cent.

Part 8: Frequently Asked Questions

Can I settle my car finance early?

Yes, but check your agreement for early settlement penalties. Some lenders charge a penalty to recover the interest they would have earned.

What happens if I miss a payment?

You'll likely be charged a default administration fee (capped by the NCA). The lender may also report the missed payment to credit bureaus, which will hurt your credit score. Multiple missed payments could lead to repossession.

Can the bank repossess my car without warning?

No. The lender must follow legal procedures, including giving you notice of default and an opportunity to catch up on payments.

What is credit life insurance, and do I need it?

Credit life insurance pays off your car loan if you die, become disabled, or are retrenched. It's not legally required, but most lenders will strongly encourage it. The NCA regulates the cost of credit life insurance.

Can I finance a car if I'm under debt review?

Traditional bank finance is generally not available while under debt review. However, some rent-to-own programmes may be an option—but you must inform your debt counsellor first.

Final Thoughts

Car finance in South Africa doesn't have to be scary. The National Credit Act provides strong protections for consumers—but those protections only work if you know about them.

The recent court cases I've covered in this guide show that the law is on your side. Lenders cannot invent fees, cannot charge unlimited interest, and cannot take your assets without following the rules.

Your job is simple: read before you sign, ask questions, and don't let anyone rush you into a deal you don't fully understand.

Because the best car deal isn't the one with the lowest monthly payment. It's the one you can actually afford to keep.

References

-

Moneyweb, "Another slapdown for banks in high court" (July 2025)

-

Business Tech Africa, "South African SARB Expected to Hold Rates Today" (March 2026)

-

GWM Edenvale, "Everything You Need To Know About Financing A Car In South Africa" (2025)

-

South African Lawyer, "SCA flags firm's 'loan shark' activities" (April 2025)

-

The Daily Sun, "Another Setback for Banks in High Court" (July 2025)

-

MQL5, "SARB Prime Rate 2025-2026"

-

SAFLII, National Credit Regulator v National Consumer Tribunal and Others [2025] ZASCA 132 (September 2025)

-

NFOSA, "CR287 Loans Loan – against policy as security" (October 2009)

-

Polity, "The Road Ahead: SCA Clears Path for Car Finance 'On the Road' Fees" (October 2025)

Guides

Reviews