The Complete Guide to Car Insurance in South Africa

The Complete Guide to Car Insurance in South Africa

Everything You Need to Know About Cover, Costs, Claims, and Your Legal Rights

Let me tell you something that might shock you.

Of the more than 11 million registered vehicles driving on South African roads, an estimated 60 to 70% are uninsured. That means when you're driving down the highway, six or seven out of every ten cars around you have no insurance whatsoever.

Now imagine this: someone without insurance runs into you. Their car is a write-off. Yours is badly damaged. Who pays for your repairs?

You do. Unless you have insurance.

I've watched this happen to friends. The other driver apologises, shrugs, and drives away in a beat-up car that they clearly never cared about. My friend is left with R80,000 in damage and no way to recover that money because the other driver has no assets worth claiming against.

This guide is going to walk you through everything you need to know about car insurance in South Africa. What the law requires (and doesn't require), what the different types of cover mean for your wallet, how insurers calculate your premium, and most importantly – what to do when things go wrong.

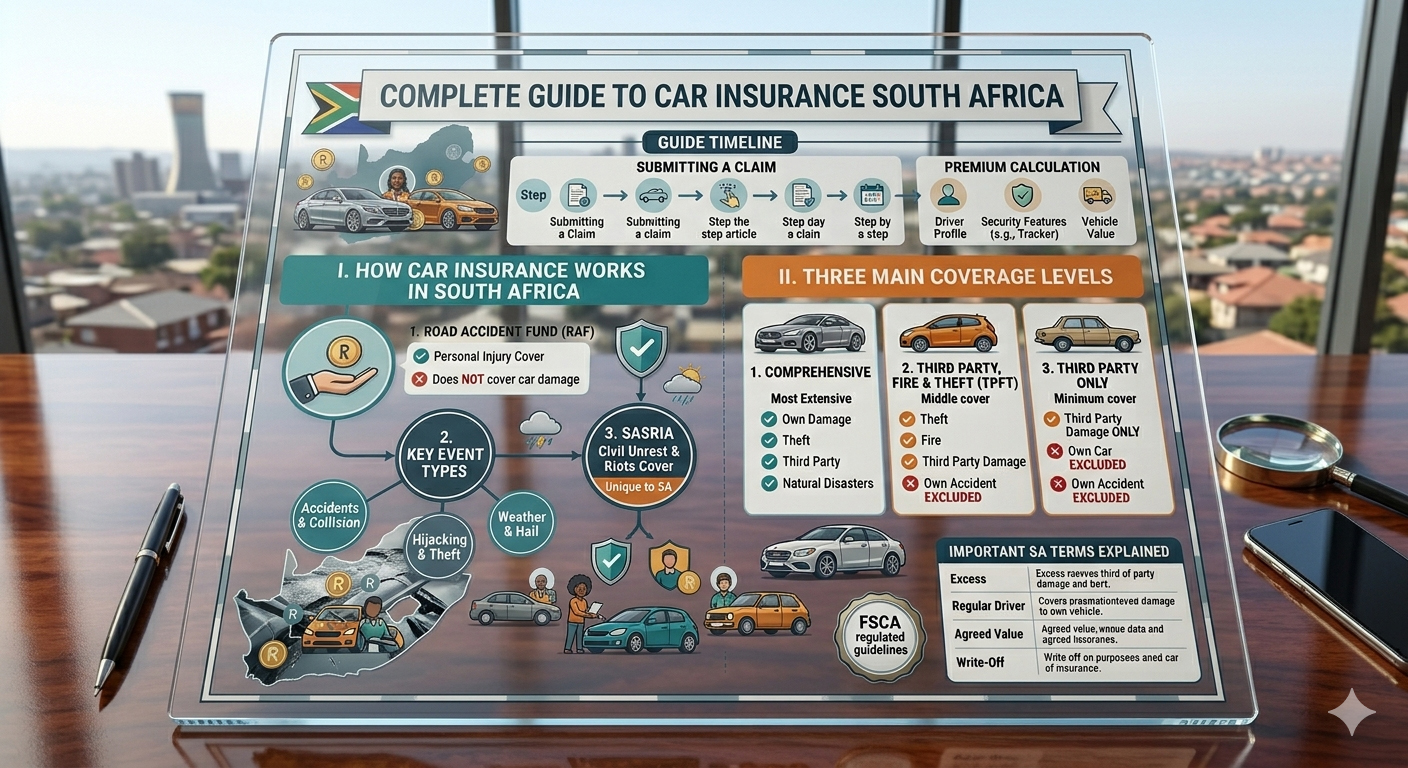

Part 1: Is Car Insurance Legally Required in South Africa?

Here's the short answer: No, the law does not require every driver to have car insurance.

You cannot be arrested or fined simply for driving without insurance. Unlike some countries where insurance is mandatory for all vehicles, South Africa takes a different approach.

But – and this is a big "but" – there are critical exceptions:

Situation Is Insurance Required?

Private vehicle, fully paid off, owned outright No, but strongly recommended Vehicle purchased with bank finance or a loan Yes – mandatory by the bank Public transport vehicles (taxis, buses) Yes, third-party liability required Vehicles carrying dangerous goods Yes

If you're financing your car, the bank holds the title and requires comprehensive insurance as a condition of the loan. They want to protect their asset. If you let your insurance lapse, the bank will likely force-place expensive cover and add it to your monthly payment.

What About the Road Accident Fund (RAF)?

The RAF provides compensation for personal injury caused by motor vehicle accidents, regardless of who was at fault. But here's what the RAF does not cover:

-

Damage to your vehicle

-

Damage to someone else's vehicle

-

Damage to property (buildings, fences, street poles)

-

Any economic losses

The RAF only covers medical expenses, loss of income, and compensation for death or serious injury. Your car's bodywork is entirely your problem.

Part 2: The Three Main Types of Car Insurance

Let me break down your options clearly. Each type has a different level of protection and a different price tag.

Type 1: Third-Party Only (Basic Cover)

What it covers:

-

Damage you cause to another person's vehicle

-

Damage you cause to someone else's property (walls, fences, buildings)

-

Injury to other people (though the RAF also covers this)

What it does NOT cover:

-

Any damage to YOUR vehicle

-

Theft of your vehicle

-

Fire damage to your vehicle

-

Your own injuries

-

Windscreen damage

Who it's for: This is the cheapest option, but it leaves you exposed. If you drive an old car worth R30,000 and you're willing to walk away from it if something happens, third-party might make sense.

Real example: Susan has third-party insurance. She crashes into another car and then hits a shopfront. Her insurer pays for the other car and the building repairs. Susan pays for her own car repairs out of pocket.

Type 2: Third-Party, Fire, and Theft

What it covers:

-

Everything third-party covers

-

Loss of your vehicle due to theft or hijacking

-

Fire damage to your vehicle

What it does NOT cover:

-

Damage to YOUR vehicle from an accident (unless it's theft or fire-related)

-

Vandalism or attempted theft (unless it results in fire)

Who it's for: This is a middle-ground option. Older cars often have electrical problems that can cause fires. Theft is a major concern in South Africa. If your car isn't worth full comprehensive but you still want protection against total loss from theft or fire, this could work.

Type 3: Comprehensive Cover

What it covers:

-

Everything from third-party, fire, and theft

-

Accident damage to YOUR vehicle, regardless of who is at fault

-

Vandalism and attempted theft damage

-

Often includes windscreen cover

-

May include roadside assistance and towing

What it typically does NOT cover:

-

Normal wear and tear

-

Mechanical breakdowns

-

Damage from driving under the influence

-

Driving with a suspended or invalid licence

-

Commercial use if you have a domestic policy

Who it's for: Most financed cars require comprehensive cover. If your car has significant value (more than R80,000–R100,000), comprehensive is usually worth the extra cost. The peace of mind alone is valuable.

Comparison Summary

Feature Third-Party Third-Party + Fire/Theft Comprehensive

Damage to others' cars ✓ ✓ ✓ Damage to property ✓ ✓ ✓ Theft of your car ✗ ✓ ✓ Fire damage ✗ ✓ ✓ Accident damage to YOUR car ✗ ✗ ✓ Vandalism ✗ ✗ ✓ Monthly premium Lowest Medium Highest Best for Older, low-value cars Older cars in high-theft areas Financed or valuable cars

Part 3: How Your Insurance Premium Is Calculated

Have you ever wondered why your neighbour pays less than you for similar cover? Here's what insurers actually look at.

The New Factor: Power-to-Weight Ratio

Modern insurers are getting more sophisticated. Some now consider your vehicle's power-to-weight (PTW) ratio when setting premiums.

Sumarie Greybe, co-founder of Naked Insurance, explains: "The power-to-weight ratio reflects how much power a vehicle produces relative to its weight. This may indicate how the vehicle will perform on the road, which in turn affects its risk profile".

A car with a higher PTW ratio can accelerate quickly and achieve higher speeds, which insurers associate with higher accident risk. But don't panic if you own a sporty car – Greybe notes that PTW ratio only has a "typically moderate" effect on premiums.

Factors That Drive Your Premium

Factor How It Affects Your Premium

Your age Younger drivers (under 25) statistically have more accidents How long you've had your licence New drivers are higher risk Your claims history Previous claims suggest future claims Where you live and park High-theft areas = higher premiums Your car's make and model Some cars are stolen more often or cost more to repair Your credit score Used as a proxy for predicting behaviour How you use the car Business use or high mileage = higher risk Security features Trackers, immobilisers, alarms can reduce premiums

Common Myths About Premiums

Myth 1: "My premium will drop automatically when I turn 25"

Not necessarily. While age is a factor, it's not the only one. Your driving history, claims record, and where you live matter just as much. There's no magic birthday where premiums suddenly plummet.

Myth 2: "Red cars cost more to insure"

False. Standard factory colours don't affect your premium. However, custom paint jobs (matte finishes, pearlescent colours, non-standard shades) can increase your premium because they cost more to repair. Always disclose modifications to your insurer.

Myth 3: "A tracker guarantees lower premiums"

Trackers can help, but the impact varies by insurer. Some offer significant discounts for approved tracking devices; others offer modest reductions. Ask your insurer specifically what kind of device qualifies and how much it saves you.

Part 4: The Roadworthiness Requirement – What Insurers Don't Always Tell You

This is one of the most important sections of this guide. Read it carefully.

Most insurance policies include a condition that your vehicle must be roadworthy at all times. If your car's poor condition causes or contributes to an accident, your insurer can legally reject your claim.

Edite Teixeira-Mckinon, Lead Ombud of the Non-life Insurance Division of the NFO, explains:

"Generally, insurance companies provide cover on the condition that the insured party takes reasonable steps to prevent harm. Most policies explicitly state that claims may be denied if the insured fails to comply with the National Road Traffic Act and the vehicle is not roadworthy at the time of the incident".

The Most Common Reasons Claims Are Rejected

Two issues top the list:

-

Worn tyres – tread depth below the legal minimum of 1.6mm

-

Faulty brakes – worn pads, leaking lines, or uneven braking

Real Case Studies from the Ombud

Case 1: The Aquaplaning Incident

A driver lost control of his vehicle when driving through a puddle of water. He claimed for accident damage. The insurer's expert found that the left rear tyre was unroadworthy – the tread wear indicators were level with the remaining tread pattern.

The expert concluded that the worn tyre could not disperse the water that the front tyres were channeling toward the rear. The car aquaplaned, and the driver lost control.

The outcome: The claim was rejected, and the NFO upheld the rejection. The unroadworthy tyre was the proximate cause of the accident.

Case 2: The Worn Brakes That Didn't Matter

A driver swerved to avoid a pothole, and his vehicle fell onto its side. He claimed for damages. The insurer rejected the claim, citing worn brake shoes and a worn rear brake disc.

The outcome: The NFO overturned the rejection. Why? Because the driver never applied the brakes during the incident – he swerved. The insurer could not prove that the brake condition was material to how the accident happened.

Key Takeaway

For an insurer to reject your claim based on unroadworthiness, they must prove that the defect caused or contributed to the accident. It's not enough to simply point out that your car has issues. However, if the defect plausibly played a role, you could be left with no cover and a massive repair bill.

How to Protect Yourself

-

Regular maintenance – Follow your manufacturer's service schedule

-

Check your tyres monthly – Use the match test (insert a match horizontally between treads; if it's level with the tread, you're borderline)

-

Test your brakes – Listen for squealing, feel for pulling, watch for warning lights

-

Keep records – Service receipts and repair documentation can prove you maintained your vehicle

Part 5: When Things Go Wrong – Your Rights and the Ombud

Disputes with insurers are common. But you have powerful rights and a free avenue for resolution.

How Common Are Insurance Disputes?

In 2024, the National Financial Ombud Scheme (NFO) handled approximately 38,855 insurance complaints. They successfully recovered R328.5 million for consumers, much of which came from short-term claims like car accidents.

The breakdown of dispute types:

-

Motor insurance: 42% of cases (the most common category)

-

Home contents: 27%

-

Building insurance: 25%

-

Life insurance: 15%

What Is the NFO?

The National Financial Ombud Scheme (NFO) was launched on 1 March 2024, consolidating several former ombuds including the Ombudsman for Short-Term Insurance (OSTI), the Ombudsman for Long-Term Insurance (OLTI), the Ombudsman for Banking Services (OBS), and the Credit Ombud.

What the NFO does:

-

Provides free, independent dispute resolution

-

Makes decisions based on law and principles of fairness and equity

-

Issues rulings that insurers must abide by (if you accept the decision)

-

Cannot procure evidence or investigate on your behalf – you must provide your evidence

What the NFO does NOT do:

-

Act as a court of law

-

Represent you in disputes

-

Charge you for their services

Step-by-Step: How to Dispute an Insurance Decision

Step 1: Contact your insurer directly

Before involving the NFO, try to resolve the issue with your insurer. Follow their formal complaints process. Get everything in writing.

Step 2: File a formal complaint

If direct communication fails, submit a written complaint to your insurer detailing the issue with supporting documents. Keep records of everything.

Step 3: Escalate to the NFO

If your insurer's final response doesn't resolve the issue, you can complain to the NFO. You'll need to complete their prescribed application form and provide:

-

Your name, policy number, and contact details

-

A factual summary of your complaint

-

Copies of all correspondence with your insurer

-

Supporting documents (repair quotes, photos, police case numbers)

Contact information:

-

Phone: 0860 800 900

-

Email: info@nfosa.co.za

The NFO Process Timeline

Phase Duration

Acknowledgement of complaint Immediate Insurer response period 21 working days Investigation and ruling 90 days (typical for complex cases)

What If the NFO Rules Against You?

The NFO's service is free and impartial, but you're not forced to accept their decision. If you disagree with the outcome, you have options:

-

Mediation – An informal process to reach a settlement

-

Small Claims Court – For disputes up to R20,000 (no lawyers required)

-

Arbitration – A binding decision from an impartial arbitrator

-

Formal court action – For larger claims, consult a lawyer first

Part 6: What to Do Immediately After an Accident

Your behaviour after an accident can affect your insurance claim. Here's what to do.

At the Scene

-

Stop immediately – Leaving the scene is a criminal offence

-

Check for injuries – Call an ambulance if needed

-

Take photos – Vehicle positions, damage, road conditions, licence plates

-

Exchange details – Names, contact info, insurance details, vehicle registrations

-

Get witness information – Names and phone numbers

-

Report to police – Required if anyone is injured or damage is significant

When Claiming

-

Notify your insurer as soon as possible – Most policies have time limits

-

Don't admit fault – Let the insurer determine liability

-

Don't authorise repairs – Wait for your insurer's assessment

-

Keep damaged parts – Insurers may want to inspect them

Part 7: Frequently Asked Questions

Do I really need insurance if my car is paid off?

Legally, no. But practically, can you afford to replace your car out of pocket if it's stolen or written off? That's the question only you can answer.

What happens if an uninsured driver hits me?

If you have comprehensive insurance, your insurer will cover your repairs and then try to recover the costs from the at-fault driver. If you only have third-party cover, you're responsible for your own repairs and must sue the other driver directly.

How much car insurance do I need?

A good rule of thumb: If you couldn't afford to replace your car tomorrow without financial hardship, you need comprehensive insurance.

Does my credit score affect my car insurance premium?

Yes. Some insurers use credit scores as a proxy for predicting behaviour. A better credit score can lead to lower premiums.

What's the difference between excess and premium?

-

Premium – What you pay monthly or annually for coverage

-

Excess – What you pay out of pocket when you make a claim

A higher excess typically means a lower premium, and vice versa.

Final Thoughts

Car insurance in South Africa isn't legally required for most private vehicles. But driving without it is a gamble – and the stakes are high.

If you have a financed car, you don't have a choice. The bank requires comprehensive cover.

If your car is paid off, you have a choice to make. Third-party cover is cheap but leaves you exposed. Comprehensive cover costs more but protects your asset.

And remember this: keeping your car roadworthy isn't just about avoiding fines. It's a condition of your insurance contract. A tyre with low tread or brakes that are worn could cost you your claim when you need it most.

The NFO is there if things go wrong – free, fair, and independent. But the best dispute is the one you never have to file. Maintain your car, disclose all modifications, read your policy wording, and drive safely.

Because at the end of the day, insurance isn't about the monthly premium. It's about whether you can sleep at night knowing you're protected.

References

-

National Financial Ombud Scheme (NFOSA). "Why Your Vehicle's Unroadworthiness Could Cost You Your Insurance Cover." (October 2025)

-

MiWay Insurance. "Know Your Car Insurance Rights." (January 2025)

-

National Financial Ombud Scheme (NFOSA). "Ombudsman for Short-Term Insurance."

-

The Citizen / Randburg Sun. "Five insurance myths busted." (October 2024)

-

The Citizen / Southern Courier. "Tips to stay covered and safe on South African roads." (October 2025)

-

Pineapple. "The Different Types Of Car Insurance In South Africa: What's Best For You!" (June 2024)

-

Pineapple. "Dealing With Insurance Disputes And Complaints In South Africa." (September 2024)

-

TopAuto. "The new factor used to calculate your car insurance premium in South Africa." (August 2024)

-

African News Agency. "How vehicle maintenance affects your insurance claims." (September 2025)

-

Cars.co.za. "The difference between Comprehensive & 3rd-Party Car Insurance." (October 2024)

Guides

Reviews