How Insurance Premiums Are Calculated in South Africa

The Hidden Maths Behind What You Pay Every Month

Let me be honest with you.

Most of us look at our insurance premium every month and just accept it. Maybe we shopped around once, got a quote, and stuck with it. But have you ever wondered why your neighbour with the same car pays less than you? Or why your premium went up even though you didn't make any claims?

Here's the truth that insurers don't always explain: your premium isn't random. It's calculated using sophisticated models that predict how likely you are to have an accident and how much that accident will cost. And those models are getting more advanced every year – with artificial intelligence and machine learning now playing a growing role in determining what you pay .

This guide will walk you through exactly how insurers calculate your premium, what factors increase or decrease what you pay, and what the law says about protecting you from unfair pricing.

Part 1: What Is an Insurance Premium, Really?

Let's start with the basics.

An insurance premium is the monthly fee you pay to an insurance provider to maintain your policy. It's the cost of transferring your risk to the insurer . Instead of worrying about a R100,000 accident, you pay a predictable monthly amount, and the insurer takes on that risk.

Here's how the maths works behind the scenes:

Insurers collect premiums from thousands (or millions) of policyholders. They invest that money, and they use it to pay claims. Their goal is to charge enough in total premiums to cover:

-

All claims they expect to pay

-

Their operating costs (salaries, offices, technology)

-

A profit margin

Your individual premium is based on your "risk profile" – a statistical snapshot of how likely you are to make a claim . If the data suggests you're high-risk, you pay more. If you're low-risk, you pay less.

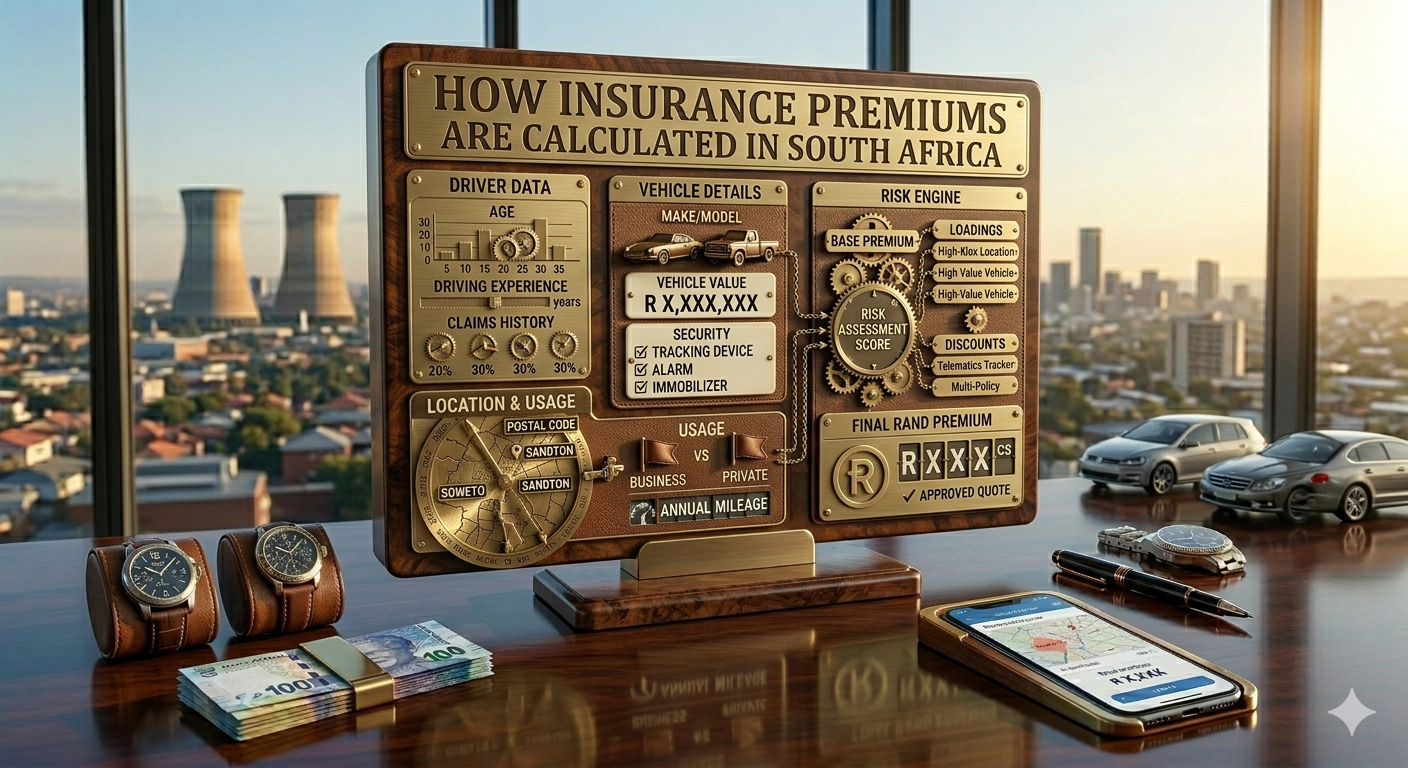

Part 2: The Main Factors That Determine Your Car Insurance Premium

Let me break down the specific factors that South African insurers look at when calculating your premium.

1. Your Vehicle's Make, Model, and Power

This is often the biggest factor. Insurers classify vehicles by risk based on:

Theft risk: Some cars are stolen more often than others. According to crime statistics, certain Toyota and Volkswagen models are frequent targets. Insurers know this, and they charge higher premiums for high-theft vehicles.

Repair costs: Luxury and imported vehicles cost more to repair. Parts may need to be ordered from overseas. Specialist labour may be required. All of this increases your premium.

The power-to-weight ratio: Here's a newer factor that many drivers don't know about. Insurers like Naked Insurance now consider your car's power-to-weight (PTW) ratio when setting premiums .

Sumarie Greybe, co-founder of Naked Insurance, explains:

"The power-to-weight ratio reflects how much power a vehicle produces relative to its weight. This may indicate how the vehicle will perform on the road, which in turn affects its risk profile."

A car with a higher PTW ratio can accelerate quickly and achieve higher speeds. In the eyes of insurers, this means it has a higher likelihood of being involved in an accident and therefore commands a higher premium .

The good news: The PTW ratio has a "typically moderate" effect on premiums. It's not the only factor, and you don't have to avoid sportier cars entirely .

2. Your Age and Driving Experience

Age is one of the most significant predictors of accident risk .

Age Group Typical Risk Level Why

Under 25 High Statistically more accidents; less driving experience 25–35 Medium-High Still developing driving habits; more night driving 35–55 Medium-Low Peak experience; more stable driving patterns 55+ Low Experienced; generally drive less aggressively

Younger drivers, particularly those under 25, typically get "slapped with a high insurance premium because they've yet to prove their experience on the road" .

Gender also matters: Statistically, male drivers pay more for car insurance than female drivers. "It has something to do with reckless driving, which is more prevalent in men than women" .

3. Your Location – Where You Live and Park

Location is crucial. Insurers consider :

-

Where you park overnight – Secure garage? Gated driveway? On-street parking?

-

Crime rates in your area – Higher theft areas mean higher premiums

-

Traffic density – Collisions are more likely in densely populated areas

-

Road quality – Potholes cause claims

If you live in a neighbourhood with high theft rates and park on the street, expect to pay significantly more than someone in a secure complex with 24-hour guards.

4. Your Driving and Claims History

Your personal history is a powerful predictor of future behaviour .

What increases your premium:

-

Previous accident claims (even if not your fault)

-

Theft claims

-

Speeding fines or other traffic violations

-

Multiple claims in a short period

What helps lower your premium:

-

A clean claims history (no claims for several years)

-

No traffic fines or violations

-

A long driving record without incidents

The new driver penalty: Having no previous insurance history can also be detrimental because insurers don't have a record of your behaviour to assess .

5. Your Credit Score

This one surprises many people. Insurers in South Africa use your credit score as "a proxy for predicting other behaviours" .

The logic is statistical: people who manage their finances responsibly tend to be more responsible in other areas of life – including driving. A better credit score generally leads to lower insurance premiums.

6. The Level of Cover You Choose

This is the factor you have the most control over .

Cover Type Premium Cost What It Covers

Third-party only Lowest Other people's damage only Third-party, fire & theft Medium Other's damage + theft and fire Comprehensive Highest Everything, including your own accident damage

The excess trade-off: Your excess (the amount you pay when you claim) has a seesaw relationship with your premium. When one goes up, the other comes down. A higher excess means a lower monthly premium .

Warning from Pineapple: "While it's all good and well to shave off R200 or R300 per month, if your excess is at R15k and you can't afford that, then what?" Always choose an excess you could actually pay in an emergency .

7. Your Security Features

Installing security devices can lower your premium:

-

Tracking devices (like Netstar or Tracker)

-

Gearlock or pedal lock

-

Alarm and immobiliser

-

Secure parking at home and work

Insurers reward you for reducing their risk.

Part 3: The Complete List of Rating Factors

Here's a comprehensive table of everything insurers consider:

Factor How It Affects Premium Notes

Car make and model High impact Theft statistics matter Car age Moderate Newer cars cost more to replace Power-to-weight ratio Moderate Higher ratio = higher premium Your age High impact Under 25 pays most Your gender Moderate Males typically pay more Years licensed High impact New drivers pay more Claims history High impact Previous claims increase premium Traffic violations Moderate Fines and offences count against you Credit score Moderate Used as behavioural proxy Parking location High impact Garage vs street matters Area crime rate High impact High-theft areas cost more Annual mileage Moderate More driving = more risk Cover type High impact Comprehensive costs most Excess amount Moderate Higher excess = lower premium Security features Low-Moderate Trackers and alarms help Bundling policies Low Multiple policies with same insurer = discount

Part 4: How Technology Is Changing Premium Calculations

The insurance industry is undergoing a quiet revolution. Traditional pricing models are being replaced by AI-driven systems that can analyse risk with far greater precision .

The Old Way vs The New Way

Traditional insurers might still factor in elements like car colour when calculating premiums. Yes, really. Some older providers still use outdated variables .

Newer insurers use sophisticated models that consider:

-

Power-to-weight ratios

-

Geospatial data (exact location risk)

-

Real-time market conditions

-

Emerging trend analysis

Ismail Canfield from insurance advisors Ctrl notes that "newer methodology would look more at factors like the driver's age, vehicle make and model, claims history, and even lately they will use a body-to-power ratio of the vehicle" .

AI and Machine Learning in Pricing

South African insurers are increasingly adopting AI-powered pricing platforms. Alpha Insure recently partnered with Akur8, a next-generation pricing platform that uses machine learning technology to :

-

Improve predictive accuracy

-

Speed up risk modelling

-

Increase market reactivity

-

Maintain transparency over pricing models

James Reid, actuarial executive at Alpha Insure, said the platform enabled them to achieve "exceptional results in risk model performance, gaining clear visibility into variables and their corresponding coefficients" .

Similarly, Ami Underwriting Managers partnered with insureAI, a South African actuarial technology firm, to drive "smarter underwriting, deliver fairer outcomes, and enhance pricing precision" .

"What this means for you," says Christelle Colman, CEO of Ami, "is the ability to offer more competitive quotes to new low-risk clients and apply smaller, more sustainable increases to existing quality policyholders" .

The Future: Fairer, More Accurate Pricing

Sumarie Greybe of Naked Insurance explains the direction of the industry:

"An exciting development is how artificial intelligence and automated systems are enabling insurers to become more precise and sophisticated in assessing how different factors affect your risk profile, ensuring that you get charged a fairer and more accurate premium" .

The goal is "rewarding responsible behaviour, enhancing customer retention, and building an insurance model centred on technical fairness and loyalty" .

Part 5: What the Law Says About Insurance Premiums

South African law provides important protections for consumers when it comes to insurance pricing. Let me walk you through the key legal framework.

The National Credit Act and Credit Life Insurance

A major legal development in 2026 affects how credit life insurance premiums can be calculated. Credit life insurance is the policy that pays off your car loan if you die, become disabled, or are retrenched.

The problem: A technical ambiguity in the Credit Life Regulations led to inconsistent industry practices .

Two different interpretations emerged:

Interpretation How It Works Consumer Impact

First interpretation Premium calculated on original loan amount and fixed for the entire term Consumers pay the same high premium even as debt decreases Second interpretation Premium calculated on outstanding balance, decreasing as debt is paid down Premiums drop over time, matching actual risk

The numbers are staggering: Consumers pay approximately R15 billion per year in credit life insurance premiums, yet insurers pay out claims of only R1.5 billion per year . That's a 10:1 ratio.

The NCR's Landmark Opinion

In March 2026, the National Credit Regulator (NCR) issued a binding opinion clarifying that the second interpretation is correct .

The NCR's opinion is based on section 106(1) of the National Credit Act, which states that credit life insurance must "at any point in time, not exceed the consumer's outstanding obligations under a credit agreement" .

In plain language: as you pay down your debt, your mandatory credit life insurance premiums should decrease accordingly.

Law firm Werksmans Attorneys explains the significance:

"In an economic environment that many believe looks set to worsen, the NCR's opinion provides consumers with some much-needed respite from credit life insurance costs that are excessive. The NCR's opinion seeks to restore coherence and fairness, and settle an ambiguity that prevailed, to the detriment of consumers" .

What This Means for You

If you have vehicle finance with mandatory credit life insurance:

-

Your premiums should be calculated on your outstanding balance, not the original loan amount

-

As you make payments, your premium should decrease progressively

-

If your insurer is using the fixed-premium approach, they are likely overcharging you

The NCR has announced it will "closely monitor the market to determine the level of compliance with its guideline and will take whatever steps are necessary to ensure compliance" .

Part 6: How to Get a Better Premium

Now that you understand how premiums are calculated, let me give you practical strategies to lower what you pay.

1. Improve Your Risk Profile

-

Drive safely – Avoid fines and violations

-

Don't claim for small amounts – Multiple claims, even small ones, increase your premium

-

Build a claims-free history – Loyalty and good behaviour are rewarded

2. Adjust Your Cover

-

Choose a higher excess – But make sure you can afford it

-

Drop comprehensive on older cars – If your car is worth under R50,000, third-party might make more sense

-

Remove unnecessary add-ons – Do you really need car hire cover?

3. Improve Your Security

-

Install a tracking device – Many insurers offer discounts

-

Park in a garage – Off-street parking reduces risk

-

Add an immobiliser or gearlock – Visible security deters thieves

4. Shop Around Regularly

-

Don't assume loyalty is rewarded – New customer discounts often beat loyalty benefits

-

Get quotes every 12-24 months – The market changes

-

Use comparison tools – See multiple options at once

5. Bundle Your Policies

-

Same insurer for car and home – Multi-policy discounts are common

-

Ask about loyalty programmes – Some insurers reward long-term customers

6. Review Your Policy Annually

As Pineapple advises: "Life changes, and so should your insurance. Regularly reviewing your policy ensures you're not overpaying for coverage you don't need" .

Part 7: Frequently Asked Questions

Why did my premium go up if I didn't make any claims?

Premiums can increase for reasons unrelated to your personal behaviour. Insurers adjust their rates based on:

-

Industry-wide claims trends

-

Rising repair costs

-

Increased theft rates for your vehicle model

-

Changes in your area's crime statistics

Does my credit score really affect my car insurance premium?

Yes. Insurers use credit scores as "a proxy for predicting other behaviours" . A better credit score generally leads to lower premiums.

Can I negotiate my premium?

You can't "haggle" like at a market, but you can:

-

Ask about available discounts

-

Request a review if your circumstances have improved (e.g., you now park in a garage)

-

Get competing quotes and ask your insurer to match them

What's the cheapest car insurance in South Africa?

The cheapest option is third-party only cover. Based on recent market data, entry-level comprehensive premiums start from approximately R350–R550 per month depending on the insurer and your risk profile . However, the cheapest is not always the best value.

How do I know if I'm being overcharged for credit life insurance?

If you have vehicle finance and your credit life premium has remained the same throughout your loan term, you may be overcharged. Contact your credit provider and ask them to explain how they calculate your premium. Reference the NCR's 2026 opinion requiring declining premiums as debt decreases .

Final Thoughts

Insurance premiums can feel like a mystery. But once you understand what goes into the calculation, you gain power.

The factors that matter most are largely within your control: your driving behaviour, where you park, your claims history, and your credit score. New technology is making pricing more accurate and fairer, rewarding responsible customers with better rates .

And the law is on your side. The NCR's 2026 opinion on credit life insurance premiums is a significant victory for consumers, ensuring that you don't pay more than you should as your debt decreases .

My advice? Review your policy today. Check your credit life premium. Compare quotes from at least three insurers. Ask questions about factors you don't understand. And remember: the cheapest premium isn't always the best value – but understanding what you're paying for is always worth the effort.

References

-

TopAuto.co.za. "The new factor used to calculate your car insurance premium in South Africa." (August 2024)

-

Insurance Biz. "Ami partners insureAI to drive precision pricing for personal lines." (May 2025)

-

Werksmans Attorneys. "NCR Throws a Lifeline to Consumers Required to Pay Premiums for Mandatory Credit Life Insurance." (March 2026)

-

Pineapple. "Car Insurance Premium Secrets Revealed: Expert Insights To Your Premiums." (September 2024)

-

FinTech Global. "Alpha Insure adopts Akur8's machine learning pricing platform for smarter underwriting." (February 2025)

-

Business Day. "Regulator clamps down on excessive credit life insurance premiums." (April 2026)

Guides

Reviews